If you’ve ever been told, “Your insurance doesn’t cover that,” you’re not alone.

For many women—especially those seeking comprehensive, personalized, root-cause care—insurance rules can feel like a brick wall. Short visits, limited options, and little room for prevention or optimization.

This is where superbills come in.

At Antigravity Wellness, we offer superbills because they support a core belief of ours:

You should be able to access the care you want and need—regardless of what your insurance company says is allowed.

__________________________________________________________________________

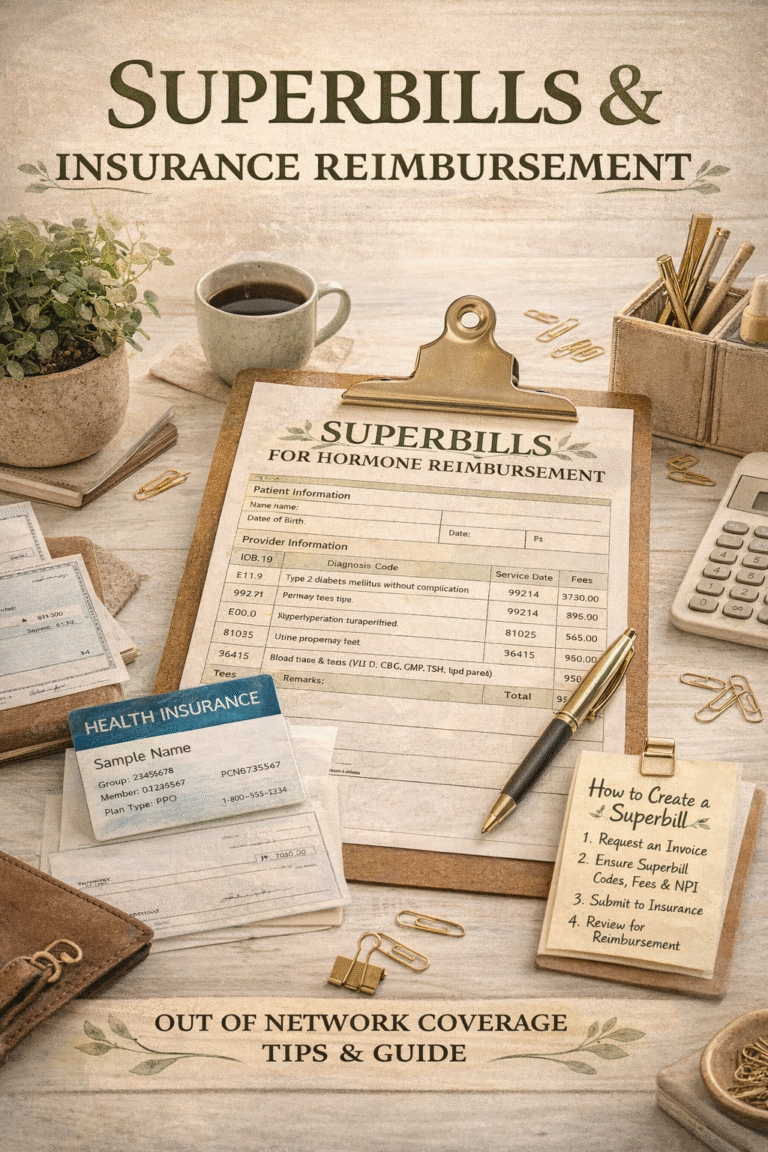

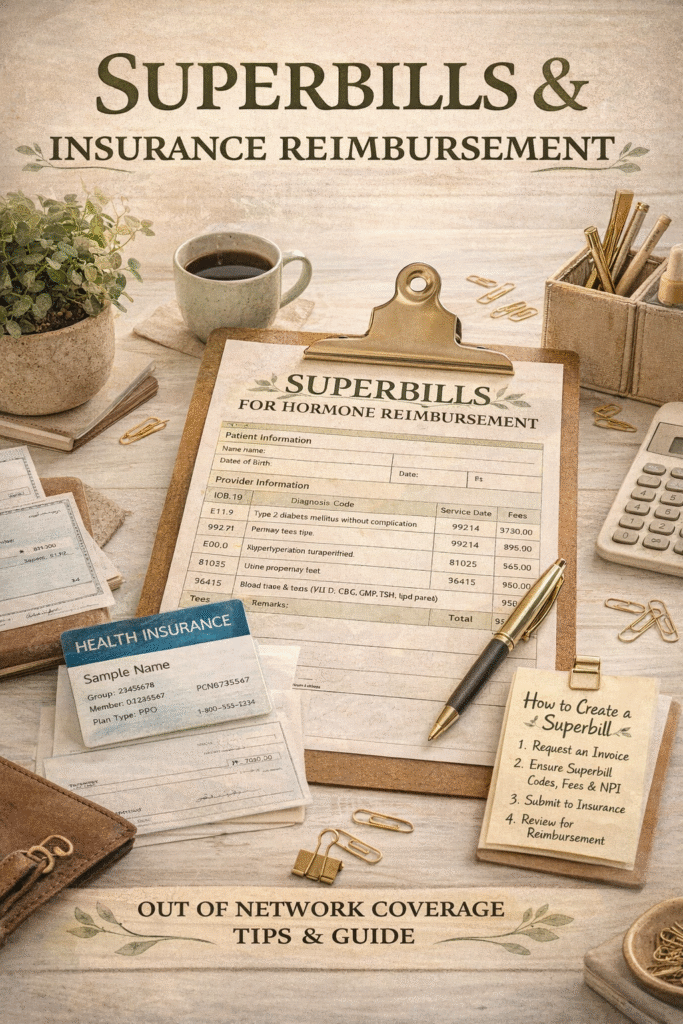

What is a superbill?

A superbill is a detailed medical receipt that includes all the information an insurance company typically requires for out-of-network reimbursement.

It may include:

Provider credentials and NPI

Practice information

Diagnostic (ICD-10) codes

Service (CPT) codes

Dates of service

Fees paid

You submit the superbill directly to your insurance company, and your insurer determines whether partial reimbursement is available based on your plan.

Important to know:

A superbill is not a guarantee of reimbursement, but many patients receive partial reimbursement, especially if they have out-of-network benefits.

__________________________________________________________________________

Why superbills matter in modern healthcare

Insurance-based healthcare was designed for:

Acute issues

Short visits

Symptom management

Standardized care

It was not designed for:

Complex hormone transitions

Chronic stress and burnout

Preventive and longevity-focused care

Time-intensive education and coaching

Root-cause medicine

Superbills create a bridge between:

The care you want

And the insurance benefits you do have

They give patients flexibility without requiring providers to practice medicine dictated by insurance rules.

__________________________________________________________________________

How superbills support patient-driven healthcare

Superbills shift power back to the patient.

Instead of insurance companies deciding:

Who you can see

How long you get

What problems are “worth” addressing

You get to:

Choose your provider

Choose a model of care that aligns with your goals

Pay for care transparently

Seek reimbursement afterward if your plan allows

This model prioritizes health outcomes, not billing efficiency.

__________________________________________________________________________

Why this works especially well for women in perimenopause & menopause

Midlife women often:

See multiple providers without clear answers

Are told symptoms are “normal” or “just stress”

Need more time, nuance, and personalization

Fall outside rigid insurance treatment pathways

Care during perimenopause and menopause frequently includes:

Detailed history-taking

Education and coaching

Functional lab interpretation

Lifestyle and nervous system support

Individualized hormone management

These services are often difficult to deliver well within insurance constraints—but superbills allow women to pursue this care anyway.

__________________________________________________________________________

How superbills are used at Antigravity Wellness

At Antigravity Wellness:

We are a self-pay practice

We do not bill insurance directly

We do provide superbills upon request for eligible services

Many of our patients have successfully used superbills to receive:

Partial reimbursement

Application toward out-of-network deductibles

Flexible use of their insurance benefits

This approach allows us to:

Spend more time with patients

Practice medicine without insurance interference

Focus on outcomes, education, and prevention

Maintain transparent pricing

__________________________________________________________________________

What superbills don’t do (important clarity)

Superbills:

❌ Do not guarantee reimbursement

❌ Do not override your insurance plan rules

❌ Do not replace HSA/FSA benefits

But they do:

Provide documentation

Create reimbursement opportunities

Expand access to care

Increase affordability for many patients

Think of superbills as an option—not a promise—and often a very helpful one.

__________________________________________________________________________

Superbills + HSA/FSA = maximum flexibility

Many patients use a combined strategy:

Pay for care using HSA or FSA funds

Submit a superbill to insurance

Receive partial reimbursement when available

This layered approach gives women:

Financial flexibility

Predictable access to care

Less dependence on insurance approval

It’s one of the smartest ways to navigate modern healthcare.

__________________________________________________________________________

Why we offer superbills (and always will)

At Antigravity Wellness, we believe:

Women deserve time, education, and partnership

Healthcare should be proactive—not crisis-driven

Insurance should not dictate the quality of care you receive

Patients should have choices

Superbills allow us to stay aligned with our values while helping patients make care more accessible.

__________________________________________________________________________

Are We a Good Fit?

If you’re considering care at Antigravity Wellness and wondering:

Whether superbills apply to you

If your insurance offers out-of-network benefits

How to combine superbills with HSA/FSA funds

The best next step is clarity.

We invite you to complete our Readiness Questionnaire, which helps determine:

Whether our model of care aligns with your goals

What level of support is appropriate

Whether now is the right time to begin

👉 Take the Readiness Questionnaire to explore next steps.

__________________________________________________________________________

References

1. Centers for Medicare & Medicaid Services (CMS). Action Plan: Bill with an out-of-network provider. https://www.cms.gov/medical-bill-rights/help/plan/insurance-provider-out-of-network

2. American Medical Association (AMA).

CPT® Code Set and Medical Billing Documentation Standards.

— Establishes standards for coding and documentation used on superbills. https://www.ama-assn.org/topics/cpt-codes

3.Consumer-Directed Health Care: Will It Improve Health System Performance? https://pmc.ncbi.nlm.nih.gov/articles/PMC1361064/

4. Buntin, M. B., et al. (2011).

Consumer-directed health care: Early evidence about effects on cost and quality.

Health Affairs, 30(6), 1039–1047. https://pubmed.ncbi.nlm.nih.gov/17062591/

5. Rosenbaum, S. (2011).

The patient protection and affordable care act: Implications for public health policy and practice.

Public Health Reports, 126(1), 130–135. https://pmc.ncbi.nlm.nih.gov/articles/PMC3001814/

__________________________________________________________________________

Medical Disclaimer

This article is for educational purposes only and is not intended to provide medical, legal, or insurance advice. Reimbursement for out-of-network services varies by insurance plan. Superbills do not guarantee reimbursement. Patients are responsible for confirming benefits with their insurance carrier. Medical services should always be discussed with a qualified healthcare professional.